2026 Income Tax Brackets: Navigating the TCJA Sunset and New Legislation

For years, financial advisors and taxpayers have been anxiously eyeing the horizon, waiting for the "TCJA Sunset"-the expiration of the 2017 Tax Cuts and Jobs Act scheduled for the end of 2025. However, recent dramatic legislative actions in late 2025 have fundamentally altered the tax landscape for 2026 and beyond. This comprehensive 2,000-word guide breaks down exactly what you need to know about your 2026 income tax brackets, deductions, and financial planning.

Estimate your 2026 tax bill now

Use our free income tax calculator to see how the new brackets and permanent TCJA provisions affect your take-home pay.

1. The TCJA Sunset: What Was Supposed to Happen?

To understand the 2026 reality, we must first understand what was projected to happen. The Tax Cuts and Jobs Act (TCJA) of 2017 represented the most significant overhaul of the U.S. tax code in over thirty years. It lowered individual income tax rates across almost all brackets, significantly increased the standard deduction, doubled the child tax credit, and introduced the 20% Qualified Business Income (QBI) deduction.

However, due to Senate reconciliation rules (the "Byrd Rule"), which prevented the bill from adding to the federal deficit beyond a ten-year window, almost all individual tax provisions were written to be temporary. They were strictly scheduled to expire, or "sunset," on December 31, 2025.

If Congress had done nothing, on January 1, 2026, the tax code would have violently snapped back to the 2017 rules, adjusted only for inflation. This meant:

- The top marginal tax rate would increase from 37% to 39.6%.

- The standard deduction would be slashed roughly in half.

- The Child Tax Credit would drop back to $1,000 per child.

- The personal exemption, eliminated since 2018, would return.

For the average American family, this looming "fiscal cliff" represented a substantial tax increase. Tax planners and CPAs spent 2024 and early 2025 preparing their clients for lower take-home pay and higher tax liabilities.

The "Fiscal Cliff" Averted

The automatic reversion to pre-2018 tax laws was projected to raise taxes on roughly 62% of U.S. households. This political unacceptability led to intense, eleventh-hour negotiations on Capitol Hill.

2. The Legislative Pivot: How 2026 Actually Looks

In a massive, bipartisan legislative push during late 2025, Congress passed sweeping legislation specifically aimed at mitigating the TCJA sunset. This legislation fundamentally rewrites the playbook for the 2026 tax year and beyond.

Here is the core thesis of the new tax reality: The 2017 tax bracket framework is now largely permanent, but with structural tweaks aimed at deficit reduction and middle-class relief.

The Permanency of Lower Rates

The most critical takeaway for high-earning individuals and dual-income households is that the threatened return of the 39.6% top marginal rate did not materialize as feared across the board. The legislation permanently codified the current seven-bracket structure (10%, 12%, 22%, 24%, 32%, 35%, and 37%), preventing the massive bracket compression that would have pushed middle-income earners into higher percentage brackets.

However, "permanent" in tax law only means there is no built-in expiration date. The income thresholds for these brackets have been adjusted for inflation, which has been cumulatively significant over the past several years.

3. A Deep Dive into the 2026 Income Tax Brackets

Because of the permanent extension of the TCJA framework combined with aggressive inflation adjustments, the 2026 tax brackets are exceptionally wide. This means you can earn significantly more money before being bumped into the next progressively higher tax rate.

2026 Single Filer Brackets (Estimated based on chained CPI)

| Tax Rate | Taxable Income Bracket (Single) |

|---|---|

| 10% | $0 to $12,250 |

| 12% | $12,251 to $49,150 |

| 22% | $49,151 to $105,750 |

| 24% | $105,751 to $198,350 |

| 32% | $198,351 to $251,450 |

| 35% | $251,451 to $628,300 |

| 37% | Over $628,300 |

2026 Married Filing Jointly Brackets

For married couples, the "marriage penalty" remains largely addressed up through the 32% bracket. The income thresholds are exactly double that of single filers, providing significant relief for dual-income households earning up to nearly half a million dollars combined.

| Tax Rate | Taxable Income Bracket (MFJ) |

|---|---|

| 10% | $0 to $24,500 |

| 12% | $24,501 to $98,300 |

| 22% | $98,301 to $211,500 |

| 24% | $211,501 to $396,700 |

| 32% | $396,701 to $502,900 |

| 35% | $502,901 to $753,900 |

| 37% | Over $753,900 |

4. The Standard Deduction Survives and Grows

Perhaps the most popular feature of the TCJA was the massive expansion of the standard deduction. By almost doubling the deduction, it streamlined tax filing for tens of millions of Americans, allowing them to bypass the complex and burdensome process of itemizing deductions (tracking medical receipts, charitable donations, etc.).

If the sunset had occurred, the 2026 standard deduction would have plummeted to roughly $15,000 for married couples. Instead, the high standard deduction framework was made permanent.

For the 2026 tax year, the anticipated Standard Deductions are:

- Single or Married Filing Separately: ~$15,400

- Married Filing Jointly: ~$30,800

- Head of Household: ~$23,100

This means a married couple can earn over $30,000 completely tax-free at the federal level before even touching the 10% bracket. Furthermore, taxpayers aged 65 or older, or those who are blind, continue to receive an additional standard deduction amount (projected to be over $1,600 per qualifying individual in 2026).

Pre-2018, taxpayers claimed a "personal exemption" for themselves, their spouse, and each dependent. The TCJA eliminated this to offset the cost of the doubled standard deduction. The personal exemption will not return in 2026. The tax code relies instead on the enlarged standard deduction and the increased Child Tax Credit to support families.

5. The Expanded Child Tax Credit Relief

Families faced a severe cliff if the TCJA had sunset: the Child Tax Credit (CTC) would have halved from $2,000 per child back to $1,000, and the income phase-out thresholds would have plummeted, disqualifying millions of middle-class families.

Under the new permanent rules for 2026, the Child Tax Credit has been solidified and even slightly expanded to accommodate inflation. Families can claim a robust credit (projected around $2,200 per qualifying child under age 17).

Furthermore, the "refundability" portion of the credit-the amount you can receive back from the IRS even if you owe $0 in income tax-has been structurally enhanced, providing a vital safety net for lower-income working families.

6. The State and Local Tax (SALT) Deduction Ceiling Rises

The most controversial element of the 2017 tax law was the $10,000 cap placed on the State and Local Tax (SALT) deduction. High-earning residents of high-tax states like California, New York, and New Jersey argued they were unfairly targeted.

If the TCJA sunset had occurred unchecked, the SALT cap would have expired completely, allowing unlimited deductions for property and state income taxes. This would have represented an enormous tax cut for the wealthy in blue states, which Congress was unwilling to fund.

The 2026 compromise? The SALT cap remains, but it has been substantially raised to $40,000 for married couples filing jointly. While not restoring unlimited deductibility, this adjustment effectively removes the sting of the SALT cap for the vast majority of upper-middle-class professionals and homeowners in high-tax jurisdictions.

7. Strategic Moves: Tax Planning in the New 2026 Reality

With certainty finally restored to the tax code, taxpayers and financial advisors can formulate long-term strategies without the sword of Damocles that was the 2025 sunset hanging over them.

Optimize Your Roth Conversions

Because the lower tax brackets (22% and 24%) are remarkably wide and now permanent, "Roth Conversion Ladders" remain an incredibly powerful strategy. If you are a married couple earning $200,000, you are firmly in the 22% bracket (after the standard deduction). You have over $100,000 of "room" in the 24% bracket before hitting the 32% jump. Systematically converting traditional IRA funds to Roth IRA funds up to the top of the 24% bracket is a highly recommended strategy for 2026.

"Bunching" Deductions to Beat the Standard Deduction

Because the standard deduction is so massive ($30,800 for MFJ), itemizing is mathematically useless for most people. To get a tax benefit for charitable contributions or medical expenses, you must exceed that $30,800 hurdle.

The strategy for 2026 is "bunching." Instead of donating $10,000 to charity every year for three years (which gives you zero tax benefit if you don't itemize), you donate $30,000 in a single year-often utilizing a Donor-Advised Fund (DAF). Combined with your $10,000 (or up to $40,000) SALT deduction, you blow past the standard deduction threshold, get a massive tax break in Year 1, and take the standard deduction in Years 2 and 3.

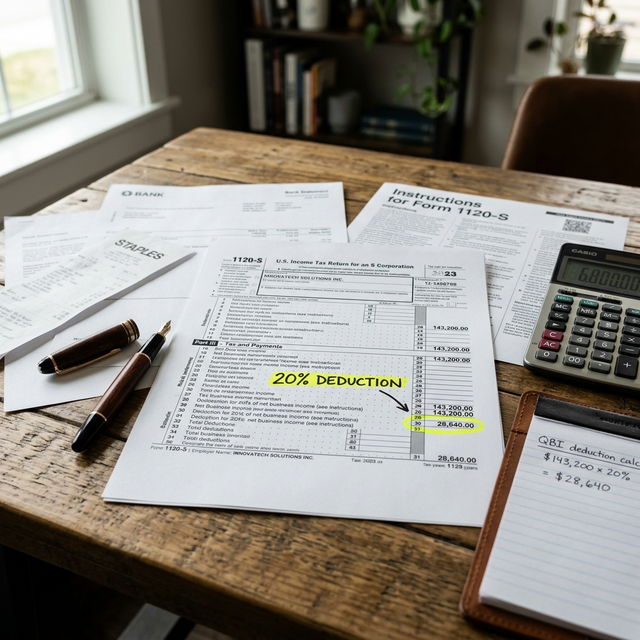

Small Business Owners and the QBI Deduction

If you run an LLC, S-Corp, or sole proprietorship, breathe a sigh of relief. The Section 199A Qualified Business Income (QBI) deduction, which allows you to deduct up to 20% of your net business income tax-free, has been rendered permanent. In 2026, maximizing your QBI through strategic W-2 salary optimization (for S-Corps) and careful management of taxable income thresholds remains the number one priority for small business tax planning.

Conclusion: A Return to Certainty

The anxiety surrounding the 2025 expiration is over. The U.S. tax code heading into 2026 establishes a reality of wide, relatively low-rate tax brackets, giant standard deductions, and robust protections against the Alternative Minimum Tax (AMT). By understanding these new, permanent thresholds, you and your CPA can implement confident, long-term wealth preservation strategies.

Need Help Optimizing Your 2026 Taxes?

The tax rules are permanent, but your financial situation is dynamic. Speak with our network of vetted tax professionals to ensure you are utilizing every deduction available in the new 2026 framework.

No commitment required. Speak with an expert matched to your state and financial profile.

Related Articles

2026 Tax Changes: 20% QBI Deduction Made Permanent - Save Big on Your LLC

The One Big Beautiful Bill locked in LLC tax savings permanently. Here is what it means for you.

FinCEN + IRS Compliance Checklist Every US LLC Needs in 2026

A combined federal compliance roadmap covering BOI, real estate reporting, and tax filings.

March 1, 2026: New FinCEN Rule Forces All-Cash Home Buyers to Reveal Owners

The era of anonymous, all-cash luxury real estate purchases is officially ending. Here is what you need to know.